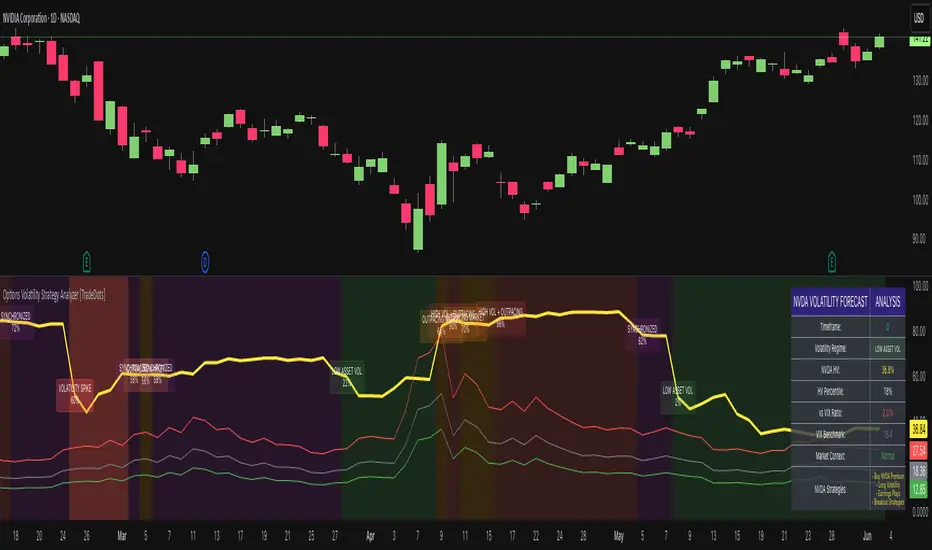

Options Volatility Strategy Analyzer [TradeDots]The Options Volatility Strategy Analyzer is a specialized tool designed to help traders assess market conditions through a detailed examination of historical volatility, market benchmarks, and percentile-based thresholds. By integrating multiple volatility metrics (including VIX and VIX9D) with color-coded regime detection, the script provides users with clear, actionable insights for selecting appropriate options strategies.

📝 HOW IT WORKS

1. Historical Volatility & Percentile Calculations

Annualized Historical Volatility (HV): The script automatically computes the asset’s historical volatility using log returns over a user-defined period. It then annualizes these values based on the chart’s timeframe, helping you understand the asset’s typical volatility profile.

Dynamic Percentile Ranks: To gauge where the current volatility level stands relative to past behavior, historical volatility values are compared against short, medium, and long lookback periods. Tracking these percentile ranks allows you to quickly see if volatility is high or low compared to historical norms.

2. Multi-Market Benchmark Comparison

VIX and VIX9D Integration: The script tracks market volatility through the VIX and VIX9D indices, comparing them to the asset’s historical volatility. This reveals whether the asset’s volatility is outpacing, lagging, or remaining in sync with broader market volatility conditions.

Market Context Analysis: A built-in term-structure check can detect market stress or relative calm by measuring how VIX compares to shorter-dated volatility (VIX9D). This helps you decide if the present environment is risk-prone or relatively stable.

3. Volatility Regime Detection

Color-Coded Background: The analyzer assigns a volatility regime (e.g., “High Asset Vol,” “Low Asset Vol,” “Outpacing Market,” etc.) based on current historical volatility percentile levels and asset vs. market ratios. A color-coded background highlights the regime, enabling traders to quickly interpret the market’s mood.

Alerts on Regime Changes & Spikes: Automated alerts warn you about any significant expansions or contractions in volatility, allowing you to react swiftly in changing conditions.

4. Strategy Forecast Table

Real-Time Strategy Suggestions: At the close of each bar, an on-chart table generates suggested options strategies (e.g., selling premium in high volatility or buying premium in low volatility). These suggestions provide a quick summary of potential tactics suited to the current regime.

Contextual Market Data: The table also displays key statistics, such as VIX levels, asset historical volatility percentile, or ratio comparisons, helping you confirm whether volatility conditions warrant more conservative or more aggressive strategies.

🛠️ HOW TO USE

1. Select Your Timeframe: The script supports multiple timeframes. For short-term trading, intraday charts often reveal faster shifts in volatility. For swing or position trading, daily or weekly charts may be more stable and produce fewer false signals.

2. Check the Volatility Regime: Observe the background color and on-chart labels to identify the current regime (e.g., “HIGH ASSET VOL,” “LOW VOL + LAGGING,” etc.).

3. Review the Forecast Table: The table suggests strategy ideas (e.g., iron condors, long straddles, ratio spreads) depending on whether volatility is elevated, subdued, or spiking. Use these as a starting point for designing trades that match your risk tolerance.

4. Combine with Additional Analysis: For optimal results, confirm signals with your broader trading plan, technical tools (moving averages, price action), and fundamental research. This script is most effective when viewed as one component in a comprehensive decision-making process.

❗️LIMITATIONS

Directional Neutrality: This indicator analyzes volatility environments but does not predict price direction (up/down). Traders must combine with directional analysis for complete strategy selection.

Late or Missed Signals: Since all calculations require a bar to close, sharp intrabar volatility moves may not appear in real-time.

False Positives in Choppy Markets: Rapid changes in percentile ranks or VIX movements can generate conflicting or premature regime shifts.

Data Sensitivity: Accuracy depends on the availability and stability of volatility data. Significant gaps or unusual market conditions may skew results.

Market Correlation Assumptions: The system assumes assets generally correlate with S&P 500 volatility patterns. May be less effective for:

Small-cap stocks with unique volatility drivers

International stocks with different market dynamics

Sector-specific events disconnected from broad market

Cryptocurrency-related assets with independent volatility patterns

RISK DISCLAIMER

Options trading involves substantial risk and is not suitable for all investors. Options strategies can result in significant losses, including the total loss of premium paid. The complexity of options strategies requires thorough understanding of the risks involved.

This indicator provides volatility analysis for educational and informational purposes only and should not be considered as investment advice. Past volatility patterns do not guarantee future performance. Market conditions can change rapidly, and volatility regimes may shift without warning.

No trading system can guarantee profits, and all trading involves the risk of loss. The indicator's regime classifications and strategy suggestions should be used as part of a comprehensive trading plan that includes proper risk management, directional analysis, and consideration of broader market conditions.

Wyszukaj w skryptach " TABLE "

MVRV Ratio [Alpha Extract]The MVRV Ratio Indicator provides valuable insights into Bitcoin market cycles by tracking the relationship between market value and realized value. This powerful on-chain metric helps traders identify potential market tops and bottoms, offering clear buy and sell signals based on historical patterns of Bitcoin valuation.

🔶 CALCULATION The indicator processes MVRV ratio data through several analytical methods:

Raw MVRV Data: Collects MVRV data directly from INTOTHEBLOCK for Bitcoin

Optional Smoothing: Applies simple moving average (SMA) to reduce noise

Status Classification: Categorizes market conditions into four distinct states

Signal Generation: Produces trading signals based on MVRV thresholds

Price Estimation: Calculates estimated realized price (Current price / MVRV ratio)

Historical Context: Compares current values to historical extremes

Formula:

MVRV Ratio = Market Value / Realized Value

Smoothed MVRV = SMA(MVRV Ratio, Smoothing Length)

Estimated Realized Price = Current Price / MVRV Ratio

Distance to Top = ((3.5 / MVRV Ratio) - 1) * 100

Distance to Bottom = ((MVRV Ratio / 0.8) - 1) * 100

🔶 DETAILS Visual Features:

MVRV Plot: Color-coded line showing current MVRV value (red for overvalued, orange for moderately overvalued, blue for fair value, teal for undervalued)

Reference Levels: Horizontal lines indicating key MVRV thresholds (3.5, 2.5, 1.0, 0.8)

Zone Highlighting: Background color changes to highlight extreme market conditions (red for potentially overvalued, blue for potentially undervalued)

Information Table: Comprehensive dashboard showing current MVRV value, market status, trading signal, price information, and historical context

Interpretation:

MVRV ≥ 3.5: Potential market top, strong sell signal

MVRV ≥ 2.5: Overvalued market, consider selling

MVRV 1.5-2.5: Neutral market conditions

MVRV 1.0-1.5: Fair value, consider buying

MVRV < 1.0: Potential market bottom, strong buy signal

🔶 EXAMPLES

Market Top Identification: When MVRV ratio exceeds 3.5, the indicator signals potential market tops, highlighting periods where Bitcoin may be significantly overvalued.

Example: During bull market peaks, MVRV exceeding 3.5 has historically preceded major corrections, helping traders time their exits.

Bottom Detection: MVRV values below 1.0, especially approaching 0.8, have historically marked excellent buying opportunities.

Example: During bear market bottoms, MVRV falling below 1.0 has identified the most profitable entry points for long-term Bitcoin accumulation.

Tracking Market Cycles: The indicator provides a clear visualization of Bitcoin's market cycles from undervalued to overvalued states.

Example: Following the progression of MVRV from below 1.0 through fair value and eventually to overvalued territory helps traders position themselves appropriately throughout Bitcoin's market cycle.

Realized Price Support: The estimated realized price often acts as a significant

support/resistance level during market transitions.

Example: During corrections, price often finds support near the realized price level calculated by the indicator, providing potential entry points.

🔶 SETTINGS

Customization Options:

Smoothing: Toggle smoothing option and adjust smoothing length (1-50)

Table Display: Show/hide the information table

Table Position: Choose between top right, top left, bottom right, or bottom left positions

Visual Elements: All plots, lines, and background highlights can be customized for color and style

The MVRV Ratio Indicator provides traders with a powerful on-chain metric to identify potential market tops and bottoms in Bitcoin. By tracking the relationship between market value and realized value, this indicator helps identify periods of overvaluation and undervaluation, offering clear buy and sell signals based on historical patterns. The comprehensive information table delivers valuable context about current market conditions, helping traders make more informed decisions about market positioning throughout Bitcoin's cyclical patterns.

Daily ATR Bonanza: Expected Moves - Tr33man Daily ATR Bonanza: Expected Moves

Overview 🤷♂️

The Daily ATR Bonanza script is a powerful trading tool designed to help traders visualize and understand potential price movements using the Average True Range (ATR). It provides daily and weekly ATR levels, historical statistics, and conditional probability analysis to give traders actionable insights. The script also plots the daily Keltner channel. This script is ideal for traders who want to gauge volatility, identify key levels, and make data-driven decisions.

b]Key Features:

📈 1. Daily and Weekly ATR Levels

🔵ATR Levels: The script calculates and displays ATR-based levels for the day and week. These levels are derived from the previous day's or week's close price and are adjusted using customizable multipliers (0.5x, 1x, and 1.5x by default).

🔵You can choose the number of ATR levels (1, 2, or 3) and adjust the multipliers to suit your trading strategy.

🌐 2. ATR Bands (Keltner Channels)

🔵The script includes an option to display ATR Bands, which are volatility-based envelopes around a moving average. These bands help identify overbought and oversold conditions.

🔵You can adjust the ATR multiplier and the length of the moving average used for the bands.

🧮 3. Historical Statistics and Conditional Probability

🔵 Historical Analysis: The script analyzes historical price movements to calculate the likelihood of closing at certain ATR levels.

🔵 Conditional Probability: This feature shows the probability of the price reaching specific ATR levels given the current market conditions. The conditional matches historical data by an open in the same opening ATR bucket, as well as the current price bucket having been visited in the historical case. Conditional probabilities are just statistics, and do not predict anything.

Data Table: 📚

🔵 Historical Close Probability: The percentage of days the price closed within each ATR level.

🔵 Conditional Close Probability: The likelihood of the price closing within each ATR level today.

❓ What is Conditional Probability? ❓

Conditional probability is a statistical measure that calculates the likelihood of an event occurring given that another event has already occurred. In this script, it is used to determine the probability of the price reaching specific ATR levels based on the current opening range as well as current ATR distance from the previous close.

For example:

If the market opens near the lower end of the first ATR level, the script calculates the likelihood of the price reaching the upper end of the first, second, or third ATR level.

This analysis is based on historical data, making it a powerful tool for understanding potential price movements.

🌟 Understanding the Levels

🔵Daily Levels: These are based on the previous day's close price and ATR. They are updated at the start of each new day.

🔵Weekly Levels: These are based on the previous week's close price and ATR. They are updated at the start of each new week.

🔵ATR Bands: These are dynamic levels that adjust with market volatility.

🔬 Analyze the Statistics (Daily only for now, no weekly yet)

🔵Use the interactive table to understand historical probabilities and conditional probabilities.

🔵Focus on the current opening range and the likelihood of reaching specific levels.

🧠 Make Trading Decisions

🔵Use the ATR levels and bands to identify key support and resistance levels.

🔵Use the conditional probability table to gauge the likelihood of reaching specific targets.

🔵Adjust your strategy based on the historical performance of the market.

Example Use Cases

1. Day Trading

Use the daily ATR levels to set intraday targets and stop-loss levels.

Monitor the conditional probability table to adjust your expectations based on the opening range.

2. Swing Trading

Use the weekly ATR levels to identify longer-term support and resistance levels.

3. Scalping

Use the ATR bands to identify overbought and oversold conditions.

Use the conditional probability table to quickly assess the likelihood of price movements.

Hippo Battlefield - Bulls VS Bears 20 bars## Hippo Battlefield – Bulls VS Bears (20 Bars)

**What it is**

A multi-dimensional momentum-and-sentiment oscillator that combines classic Bull/Bear Power with ATR- or peak-normalization, then layers on RSI and MACD-derived metrics into:

1. **A colored bar series** showing net Bull+Bear Power strength over the last 20 bars,

2. **A dynamic table** of each of those 20 BBP values (grouped into four 5-bar “quartals”), with symbols, per-bar change, and rolling averages, and

3. **A composite “Weighted BBP” histogram** blending normalized RSI, MACD, and BBP into a single view.

---

### Key Inputs

- **Length (EMA)** – look-back for the underlying EMA (default 60)

- **Normalization Length** – look-back window for peak-normalization (default 60)

- **Use ATR for Norm.** – toggle ATR-based normalization vs. highest-abs(BBP)

- **Show Tables** – toggle the bottom-right 21×11 grid of raw and average BBP values

---

### What You See

#### 1. Colored Bars (Overlay = false)

- Bars are colored by normalized BBP intensity:

- Extreme Bull (≥+10): deep blue

- Strong Bull (+5 to +10): green/yellow

- Weak Bull (+0 to +5): dark green

- Weak Bear (–0 to –5): dark red

- Strong Bear (–5 to –10): pink/red

- Extreme Bear (<–10): magenta

#### 2. Bottom-Right Table (20 Bars of Data)

- Divided into four columns (0–4, 5–9, 10–14, 15–19 bars ago) and one “average” row.

- Each cell shows:

1. Bar index (1–20),

2. Normalized BBP value (to four decimals),

3. Direction symbol (↑/↓/=),

4. Bar-to-bar change (± value),

5. A separator “|”.

- At the very bottom, each column’s 5-bar average is displayed as “Avg: X.XXXX” with a dot marker.

#### 3. Top-Center Mini-Table

- When ≥20 bars have elapsed, shows the date at 20 bars ago and the average BBP across the full 20-bar window.

#### 4. Normalized RSI Line

- Rescales the classic 14-period RSI into a –20…+20 band to align with BBP.

#### 5. MACD Lines (Hidden) & Composite Histogram

- MACD and signal lines are calculated but not plotted by default.

- A “Weighted BBP” histogram combines:

- 20% normalized RSI,

- 20% average of (MACD + signal + normalized BBP),

- 60% normalized BBP

- Plotted as columns, color-coded by strength using the same palette as the main bars.

#### 6. Middle Reference Line

- A horizontal zero line to anchor over/under-zero readings.

---

### How to Use It

- **Trend confirmation**: Strong blue/green bars alongside a rising histogram suggest bull conviction; strong reds/magentas signal bear dominance.

- **Divergence spotting**: Watch for price making new highs/lows while BBP or the histogram fails to follow.

- **Quartal analysis**: The 5-bar group averages can reveal whether recent momentum is accelerating or waning.

- **Cross-indicator weighting**: Because RSI, MACD, and raw BBP all feed into the final histogram, you get a smoothed, blended view of momentum shifts.

---

**Tip:** Tweak the EMA and normalization length to suit your preferred timeframe (e.g. shorter for intraday scalps, longer for swing trades). Enable/disable the table if you prefer a cleaner pane.

Balancelink : Partition Function 1.0This script computes the partition function values 𝑝(𝑛) using Euler’s Pentagonal Number Theorem and displays them in a horizontally wrapped table directly on the chart. The partition function is a classic function in number theory that counts the number of ways an integer 𝑛 can be expressed as a sum of positive integers, disregarding the order of the summands.

Key Features

Efficient Calculation:

The script computes 𝑝(𝑛) for all orders from 0 up to a user-defined maximum (set by the "End Order" input). The recursive computation leverages Euler’s Pentagonal Number Theorem, ensuring the function is calculated correctly for each order.

Display Range Selection:

Users can select a specific range of orders (for example, from 𝑛 = 100 to 𝑛 = 200 to display.) This means you can focus on a particular segment of the partition function results without cluttering the chart.

Horizontally Wrapped Table:

The partition values are organized into a clean, horizontal table with a customizable number of columns per row (default is 20). When the number of values exceeds the maximum columns, the table automatically wraps onto a new set of rows for better readability.

Medium Text Size:

The table cells use a medium (normal) text size for easy viewing and clarity.

How to Use

Inputs:

Start Order (n): The starting index from which you want to display the partition function (default is 100).

End Order (n): The ending index up to which the partition function values will be displayed (default is 200).

Max Columns Per Row: Determines how many results are shown per row before wrapping to the next (default is 20).

Calculation:

The script calculates all 𝑝(𝑛) values from 0 up to the specified "End Order". It then extracts and displays only the values in the chosen range.

Visualization:

The computed values are shown in a neatly arranged table at the top right of your TradingView chart, making it simple to scroll through and inspect the partition function values.

Use Cases

Educational & Research:

Ideal for educators and students exploring concepts of integer partitions and number theory.

Data Analysis & Pattern Recognition:

Useful for those interested in the behavior and growth of partition numbers as 𝑛 increases.

Geometric Momentum Breakout with Monte CarloOverview

This experimental indicator uses geometric trendline analysis combined with momentum and Monte Carlo simulation techniques to help visualize potential breakout areas. It calculates support, resistance, and an aggregated trendline using a custom Geo library (by kaigouthro). The indicator also tracks breakout signals in a way that a new buy signal is triggered only after a sell signal (and vice versa), ensuring no repeated signals in the same direction.

Important:

This script is provided for educational purposes only. It is experimental and should not be used for live trading without proper testing and validation.

Key Features

Trendline Calculation:

Uses the Geo library to compute support and resistance trendlines based on historical high and low prices. The midpoint of these trendlines forms an aggregated trendline.

Momentum Analysis:

Computes the Rate of Change (ROC) to determine momentum. Breakout conditions are met only if the price and momentum exceed a user-defined threshold.

Monte Carlo Simulation:

Simulates future price movements to estimate the probability of bullish or bearish breakouts over a specified horizon.

Signal Tracking:

A persistent variable ensures that once a buy (or sell) signal is triggered, it won’t repeat until the opposite signal occurs.

Geometric Enhancements:

Calculates an aggregated trend angle and channel width (distance between support and resistance), and draws a perpendicular “breakout zone” line.

Table Display:

A built-in table displays key metrics including:

Bullish probability

Bearish probability

Aggregated trend angle (in degrees)

Channel width

Alerts:

Configurable alerts notify when a new buy or sell breakout signal occurs.

Inputs

Resistance Lookback & Support Lookback:

Number of bars to look back for determining resistance and support points.

Momentum Length & Threshold:

Period for ROC calculation and the minimum percentage change required for a breakout confirmation.

Monte Carlo Simulation Parameters:

Simulation Horizon: Number of future bars to simulate.

Simulation Iterations: Number of simulation runs.

Table Position & Text Size:

Customize where the table is displayed on the chart and the size of the text.

How to Use

Add the Script to Your Chart:

Copy the code into the Pine Script editor on TradingView and add it to your chart.

Adjust Settings:

Customize the inputs (e.g., lookback periods, momentum threshold, simulation parameters) to fit your analysis or educational requirements.

Interpret Signals:

A buy signal is plotted as a green triangle below the bar when conditions are met and the state transitions from neutral or sell.

A sell signal is plotted as a red triangle above the bar when conditions are met and the state transitions from neutral or buy.

Alerts are triggered only on the bar where a new signal is generated.

Examine the Table:

The table displays key metrics (breakout probabilities, aggregated trend angle, and channel width) to help evaluate current market conditions.

Disclaimer

This indicator is experimental and provided for educational purposes only. It is not intended as a trading signal or financial advice. Use this script at your own risk, and always perform your own research and testing before using any experimental tools in live trading.

Credit

This indicator uses the Geo library by kaigouthro. Special thanks to Cryptonerds and @Hazzantazzan for their contributions and insights.

Sniper TradingSniper Trader Indicator Overview

Sniper Trader is a comprehensive trading indicator designed to assist traders by providing valuable insights and alerting them to key market conditions. The indicator combines several technical analysis tools and provides customizable inputs for different strategies and needs.

Here’s a detailed breakdown of all the components and their functions in the Sniper Trader indicator:

1. MACD (Moving Average Convergence Divergence)

The MACD is a trend-following momentum indicator that helps determine the strength and direction of the current trend. It consists of two lines:

MACD Line (Blue): Calculated by subtracting the long-term EMA (Exponential Moving Average) from the short-term EMA.

Signal Line (Red): The EMA of the MACD line, typically set to 9 periods.

What does it do?

Buy Signal: When the MACD line crosses above the signal line, it generates a buy signal.

Sell Signal: When the MACD line crosses below the signal line, it generates a sell signal.

Zero Line Crossings: Alerts are triggered when the MACD line crosses above or below the zero line.

2. RSI (Relative Strength Index)

The RSI is a momentum oscillator used to identify overbought or oversold conditions in the market.

Overbought Level (Red): The level above which the market might be considered overbought, typically set to 70.

Oversold Level (Green): The level below which the market might be considered oversold, typically set to 30.

What does it do?

Overbought Signal: When the RSI crosses above the overbought level, it’s considered a signal that the asset may be overbought.

Oversold Signal: When the RSI crosses below the oversold level, it’s considered a signal that the asset may be oversold.

3. ATR (Average True Range)

The ATR is a volatility indicator that measures the degree of price movement over a specific period (14 bars in this case). It provides insights into how volatile the market is.

What does it do?

The ATR value is plotted on the chart and provides a reference for potential market volatility. It's used to detect flat zones, where the price may not be moving significantly, potentially indicating a lack of trends.

4. Support and Resistance Zones

The Support and Resistance Zones are drawn by identifying key swing highs and lows over a user-defined look-back period.

Support Zone (Green): Identifies areas where the price has previously bounced upwards.

Resistance Zone (Red): Identifies areas where the price has previously been rejected or reversed.

What does it do?

The indicator uses swing highs and lows to define support and resistance zones and highlights these areas on the chart. This helps traders identify potential price reversal points.

5. Alarm Time

The Alarm Time feature allows you to set a custom time for the indicator to trigger an alarm. The time is based on Eastern Time and can be adjusted directly in the inputs tab.

What does it do?

It triggers an alert at a user-defined time (for example, 4 PM Eastern Time), helping traders close positions or take specific actions at a set time.

6. Market Condition Display

The Market Condition Display shows whether the market is in a Bullish, Bearish, or Flat state based on the MACD line’s position relative to the signal line.

Bullish (Green): The market is in an uptrend.

Bearish (Red): The market is in a downtrend.

Flat (Yellow): The market is in a range or consolidation phase.

7. Table for Key Information

The indicator includes a customizable table that displays the current market condition (Bull, Bear, Flat). The table is placed at a user-defined location (top-left, top-right, bottom-left, bottom-right), and the appearance of the table can be adjusted for text size and color.

8. Background Highlighting

Bullish Reversal: When the MACD line crosses above the signal line, the background is shaded green to highlight the potential for a trend reversal to the upside.

Bearish Reversal: When the MACD line crosses below the signal line, the background is shaded red to highlight the potential for a trend reversal to the downside.

Flat Zone: A flat zone is identified when volatility is low (ATR is below the average), and the background is shaded orange to signal periods of low market movement.

Key Features:

Customizable Time Inputs: Adjust the alarm time based on your local time zone.

User-Friendly Table: Easily view market conditions and adjust display settings.

Comprehensive Alerts: Receive alerts for MACD crossovers, RSI overbought/oversold conditions, flat zones, and the custom alarm time.

Support and Resistance Zones: Drawn automatically based on historical price action.

Trend and Momentum Indicators: Utilize the MACD and RSI for identifying trends and market conditions.

How to Use Sniper Trader:

Set Your Custom Time: Adjust the alarm time to match your trading schedule.

Monitor Market Conditions: Check the table for real-time market condition updates.

Use MACD and RSI Signals: Watch for MACD crossovers and RSI overbought/oversold signals.

Watch for Key Zones: Pay attention to the support and resistance zones and background highlights to identify market turning points.

Set Alerts: Use the built-in alerts to notify you of buy/sell signals or when it’s time to take action at your custom alarm time.

Ichimoku(TF)This Pine Script indicator is a comprehensive Ichimoku Cloud implementation designed for TradingView. Its uniqueness lies in the precisely calculated settings for each timeframe, offering a tailored Ichimoku experience across different chart resolutions.

Key Features:

Timeframe-Specific Presets: The indicator includes a wide range of pre-defined settings optimized for various timeframes (1m, 2m, 3m, 5m, 10m, 15m, 30m, 45m, 1H, 2H, 3H, 4H, 6H, 12H, 18H, 1D, 3D, 1W, 1M). This ensures accurate Ichimoku calculations and relevant signals for your chosen timeframe.

Ichimoku Cloud: Plots the standard Ichimoku Cloud components: Tenkan-sen (Conversion Line), Kijun-sen (Base Line), Senkou Span A & B (Leading Spans), and Chikou Span (Lagging Span).

Configurable Display: Allows toggling the Ichimoku Cloud display, coloring bars based on the trend (above or below the cloud), and customizing table visibility, style, font size and position.

Trend Analysis Table: A summary table provides a quick overview of the current trend based on Ichimoku components. It assesses the strength of the trend based on the price's relation to the Tenkan-sen, Kijun-sen, Kumo Cloud, Chikou Span and Kumo Twist. The table offers both detailed and short styles.

Buy/Sell Signals: Generates buy and sell signals based on Tenkan-sen/Kijun-sen crossovers.

Uniqueness:

The primary advantage of this indicator is its meticulous configuration for different timeframes. Instead of using a single set of parameters for all timeframes, it provides optimized values that are more suitable for specific chart resolutions. The summary table provides an easy and quick way to assess the trend.

Этот индикатор Pine Script представляет собой комплексную реализацию облака Ишимоку, разработанную для TradingView. Его уникальность заключается в точно рассчитанных настройках для каждого таймфрейма, предлагая индивидуальный опыт Ишимоку для различных разрешений графиков.

Ключевые особенности:

Предустановки для конкретных таймфреймов: Индикатор включает в себя широкий спектр предопределенных настроек, оптимизированных для различных таймфреймов (1m, 2m, 3m, 5m, 10m, 15m, 30m, 45m, 1H, 2H, 3H, 4H, 6H, 12H, 18H, 1D, 3D, 1W, 1M). Это обеспечивает точные вычисления Ишимоку и релевантные сигналы для выбранного вами таймфрейма.

Облако Ишимоку: Отображает стандартные компоненты облака Ишимоку: Tenkan-sen (линия конверсии), Kijun-sen (базовая линия), Senkou Span A & B (ведущие диапазоны) и Chikou Span (запаздывающий диапазон).

Настраиваемое отображение: Позволяет переключать отображение облака Ишимоку, окрашивать бары в зависимости от тренда (выше или ниже облака), а также настраивать видимость таблицы, стиль, размер шрифта и положение.

Таблица анализа тренда: Сводная таблица обеспечивает быстрый обзор текущего тренда на основе компонентов Ишимоку. Он оценивает силу тренда на основе отношения цены к Tenkan-sen, Kijun-sen, облаку Kumo, Chikou Span и Kumo Twist. Таблица предлагает как подробный, так и краткий стили.

Сигналы покупки/продажи: Генерирует сигналы покупки и продажи на основе пересечений Tenkan-sen/Kijun-sen.

Уникальность:

Основным преимуществом этого индикатора является его тщательная настройка для разных таймфреймов. Вместо использования единого набора параметров для всех таймфреймов он предоставляет оптимизированные значения, которые больше подходят для конкретных разрешений графиков. Сводная таблица обеспечивает простой и быстрый способ оценки тренда.

EMA CROSS v1.0 by ScorpioneroIndicator Description: Multi-Timeframe SMA Table & Plot

This indicator displays a structured table of Simple Moving Averages (SMA) across multiple timeframes and plots them directly on the chart for better trend analysis.

Features:

✅ Multi-Timeframe SMA Calculation: Computes SMAs for different periods (10, 60, and 223) across six timeframes (1m, 3m, 5m, 15m, 30m, 60m).

✅ Sorted SMA Table: Displays a table in the bottom-right corner of the chart, showing the three SMAs per timeframe, sorted in descending order.

✅ Color-Coded Cells: Each SMA is highlighted with a specific color:

🟡 Yellow → 10-period SMA

🔵 Blue → 60-period SMA

🟣 Purple → 223-period SMA

⚪ Gray → Other values

✅ SMA Plotting on the Chart: All calculated SMAs are plotted directly on the price chart, allowing users to visualize their interaction with price movements.

How to Use:

The table provides a quick overview of SMA rankings across timeframes, helping identify bullish or bearish trends.

The SMA plots on the chart can be used for dynamic support/resistance analysis and trend confirmation.

This indicator is ideal for traders who rely on multi-timeframe trend analysis to make informed trading decisions! 🚀

by Scorpionero

Precious Metals & GSR (Zeiierman)█ Overview

The Precious Metals & GSR (Zeiierman) is designed to provide traders and investors with a comprehensive view of the Gold-Silver Ratio (GSR) and other precious metal relationships. This tool helps evaluate the relative strength between different metals by analyzing their price ratios over historical periods, using quantile-based analysis and trend interpretation tables to highlight key insights.

The Gold-Silver Ratio (GSR) is a widely utilized metric in precious metals trading, representing the number of silver ounces required to purchase one ounce of gold. Historically, this ratio has fluctuated, providing traders with insights into the relative value of these two metals. By analyzing the GSR, traders can identify potential trading opportunities based on historical patterns and market dynamics.

By integrating customizable percentile bands, gradient coloring for performance visualization, and dynamic ratio analysis, this indicator assists in understanding how one metal is performing relative to another, making it useful for trend tracking, risk management, and portfolio allocation.

█ How It Works

The Precious Metals & GSR Indicator operates by fetching the latest prices of the selected precious metals in the user's chosen currency. It then calculates the ratio between two selected metals (Metal 1 and Metal 2) and analyzes this ratio over a specified period. By computing quantile bands and high/low bands, the indicator provides insights into the historical performance and current standing of the ratio.

⚪ Ratio Calculation

The core of this indicator is the metal ratio, calculated by dividing the price of Metal 1 by Metal 2.

A rising ratio means Metal 1 is outperforming Metal 2.

A falling ratio means Metal 2 is outperforming Metal 1.

The indicator automatically retrieves live market prices of Gold, Silver, Platinum, and Palladium to compute the ratio.

⚪ Quantile Ratio Bands

The indicator calculates the highest (max) and lowest (min) ratio levels over a user-defined period.

It also plots quantile bands at the 10th, 25th, 50th (median), 75th, and 90th percentiles, providing deeper statistical insights into how extreme or average the current ratio is.

The median (Q50) acts as a reference level, showing whether the ratio is above or below its historical midpoint.

⚪ Interpretation Table

The Ratio Interpretation Table provides a text-based summary of the ratio’s strength.

It detects whether Metal 1 is at a historical high, low, or within common ranges.

This helps traders and investors make informed decisions on whether the ratio is overextended, mean-reverting, or trending.

⚪ Precious Metals Table

Displays live market prices for Gold, Silver, Platinum, and Palladium.

Prices are shown in different units (oz, kg, grams, and troy ounces) based on user preferences.

A color-coded system highlights price changes, making it easier to track market movements.

⚪ Physical Holding Calculator

Users can enter their precious metal holdings to estimate their current value.

The system adjusts calculations based on weight, purity (24K, 22K, etc.), and unit of measurement.

The holding value is displayed in the selected currency (USD, EUR, GBP, etc.).

█ How to Use

⚪ Trend Identification

If the ratio is increasing, Metal 1 is gaining strength relative to Metal 2 → Possible Long Position on Metal 1 / Short on Metal 2

If the ratio is decreasing, Metal 2 is gaining strength relative to Metal 1 → Possible Short Position on Metal 1 / Long on Metal 2

⚪ Mean Reversion Strategy

When the ratio reaches the 90th percentile, Metal 1 is historically overextended (expensive) compared to Metal 2.

Traders may look to sell Metal 1 and buy Metal 2, expecting the ratio to decline back toward its historical average.

Example (Gold/Silver Ratio): If the GSR is above the 90th percentile, gold is very expensive relative to silver, suggesting a potential buying opportunity in silver and/or a selling opportunity in gold.

When the ratio reaches the 10th percentile, Metal 1 is historically undervalued (cheap) compared to Metal 2.

Traders may look to buy Metal 1 and sell Metal 2, expecting the ratio to rise back toward its historical average.

Example (Gold/Silver Ratio): If the GSR is below the 10th percentile, gold is very cheap relative to silver, suggesting a potential buying opportunity in gold and/or a selling opportunity in silver.

⚪ Common Strategy Based on GSR Insights

A common approach involves monitoring the ratio for extreme values based on historical data. When the ratio reaches historically high levels, it suggests that gold is expensive relative to silver, potentially indicating a buying opportunity for silver and/or a selling opportunity for gold. Conversely, when the ratio is at historically low levels, silver is expensive relative to gold, suggesting a potential buying opportunity for gold and/or selling opportunity for silver. This mean-reversion strategy relies on the tendency of the GSR to return to its historical average over time.

⚪ Hedging & Portfolio Diversification

If Gold is strongly outperforming Silver, investors may shift allocations to balance risk.

If Silver is rapidly gaining on Gold, it may indicate increased industrial demand or speculative interest.

⚪ Inflation & Economic Cycles

A rising Gold-Silver ratio often correlates with economic downturns and increased risk aversion.

A falling Gold-Silver ratio may signal stronger economic growth and higher inflation expectations.

█ Settings

Precious Metals Table

Select which metals to display (Gold, Silver, Platinum, Palladium)

Choose measurement units (oz, kg, grams, troy ounces)

Ratio Analysis

Select Metal 1 & Metal 2 for ratio calculation

Set historical length for quantile calculations

Interpretation Table

Enable automated insights based on ratio levels

Physical Holdings Calculator

Enter metal weight, purity, and unit

Select calculation currency

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

EBL - Enigma BOS Logic Select Higher Time FrameThe "EBL – Enigma BOS Logic" is a unique multi-timeframe trading indicator designed for traders who rely on structured price action and key level retests to find high-probability trade opportunities. This indicator automates the identification of significant price levels on a higher timeframe, plots them across all lower timeframes, and provides actionable signals (buy/sell) when price retests those levels. It is ideal for traders who focus on lower timeframes for precise entries while using higher timeframe structure for trend confirmation.

How the Indicator Works

Key Level Detection:

The indicator allows the user to select a key level timeframe (e.g., 1H, 4H, Daily, Weekly). It then identifies Break of Structure (BOS) levels on the selected timeframe.

When a bullish-to-bearish or bearish-to-bullish reversal is detected on the selected timeframe, the corresponding high or low of the reversal candle is stored as a key level.

These key levels are plotted as horizontal lines on all lower timeframes, helping the trader visualize critical support and resistance zones across multiple timeframes.

Retest Confirmation:

Once a key level is established, the indicator continuously monitors the price action on lower timeframes.

If the price touches or crosses a key level, it is considered a retest, and an alert is generated.

The indicator plots a retest marker (customizable as a circle or diamond) at the exact price level where the retest occurred, providing a clear visual cue for the trader.

Trading Signals:

When a retest is detected, a table is displayed on the chart with the following information:

The trading pair.

The signal direction (Buy/Sell).

The price at which the retest occurred.

This table gives traders instant insight into actionable opportunities, making it easier to focus on live market conditions without missing critical retests.

Key Features

Multi-Timeframe Analysis: The indicator focuses on a higher timeframe selected by the user, ensuring that only the most relevant key levels are plotted for lower timeframe trading.

Dynamic Retest Signals: It dynamically identifies when price retests a key level and provides both visual markers and real-time alerts.

Customizable Retest Markers: Users can customize the retest marker's shape (circle/diamond) and color to suit their preferences.

Signal Table: A built-in table displays clear buy or sell signals when retests occur, ensuring that traders have all the necessary information at a glance.

Alerts: The indicator supports real-time alerts for retests, helping traders stay informed even when they are not actively monitoring the chart.

How to Use the Indicator

Select a Key Level Timeframe:

In the input settings, choose a higher timeframe (e.g., 4H or Daily) to define key levels.

The indicator will calculate Break of Structure (BOS) levels on the selected timeframe and plot them as horizontal lines across all lower timeframes.

Monitor Lower Timeframes for Retests:

Switch to a lower timeframe (e.g., 15m, 5m) to wait for price to approach the key levels plotted by the indicator.

When a retest occurs, observe the signal table and retest marker for actionable trade signals.

Act on Buy/Sell Signals:

Use the information provided by the signal table to make trading decisions.

For a buy signal, wait for bullish confirmation (e.g., price holding above the retested level).

For a sell signal, wait for bearish confirmation (e.g., price holding below the retested level).

Trading Concepts and Underlying Logic

The indicator is based on the Break of Structure (BOS) concept, a core principle in price action trading. BOS levels represent points where the market shifts its trend direction, making them critical zones for potential reversals or continuations.

By focusing on higher timeframe BOS levels, the indicator helps traders align their lower timeframe entries with the overall market trend.

The concept of retests is used to confirm the validity of a key level. A retest occurs when the price returns to a previously identified BOS level, offering a high-probability entry point.

Use Cases

Scalping: Traders who prefer lower timeframe scalping can use the indicator to align their trades with higher timeframe key levels, increasing the likelihood of successful trades.

Swing Trading: Swing traders can use the indicator to identify key reversal zones on higher timeframes and plan their trades accordingly.

Intraday Trading: Intraday traders can benefit from the real-time alerts and signals generated by the indicator, ensuring they never miss critical retests during active trading hours.

Conclusion

The "EBL – Enigma BOS Logic" is a powerful tool for traders who want to enhance their price action trading by focusing on key levels and retests across multiple timeframes. By automating the identification of BOS levels and providing clear retest signals, it helps traders make more informed and confident trading decisions. Whether you are a scalper, intraday trader, or swing trader, this indicator offers valuable insights to improve your trading performance.

Smart Money Breakouts [iskess 01-02 11:05]This is an big update to the excellent Smart Money Breakout Script published in Oct 2023 by ChartPrime who, to my knowledge, was the original author.

FULL CREDIT GOES TO CHARTPRIME FOR THIS ORIGINAL WORK.

Per the moderator's rules, you will find below a meaningful, detailed self-contained description that does not rely on delegation to the open source code or links to other content. You will find in the description details on what the script does, how it does that, how to use it, and how it is original.

The "Smart Money Breakouts" indicator is designed to identify breakouts based on changes in character (CHOCH) or breaks of structure (BOS) patterns, facilitating automated trading with user-defined Take Profit (TP) level.

The indicator incorporates essential elements such as volume analysis and a data table to assist traders in optimizing their strategies.

🔸Breakout Detection:

The indicator scans price movements for "Change in Character" (CHOCH) and "Break of Structure" (BOS) patterns, signaling potential breakout opportunities in the market.

🔸User-Defined TP/SL :

Traders can customize the Take Profit (TP) and Stop Loss (SL) through the indicator settings, with these levels dynamically calculated based on the Average True Range (ATR). This allows for precise risk management and profit targets that adapt to market volatility. Traders can also select the lookback period for the TP/SL calculations.

🔸Volume Analysis and Trade Direction Specific Analysis:

The indicator includes a volume checker that provides valuable insights into the strength of the breakout, taking into account trade direction.

🔸If the volume label is red and the trade is long, it suggests a higher likelihood of hitting the Stop Loss (SL).

🔸If the volume label is green and the trade is long, it indicates a higher probability of hitting the Take Profit (TP).

🔸For short trades, a red volume label suggests a higher likelihood of hitting TP, while a green label suggests a higher likelihood of hitting SL.

🔸A yellow volume label suggests that the volume is inconclusive, neither favoring bullish nor bearish movements.

🔸Data Table:

The indicator features a data table that keeps track of the number of winning and losing trades for specific timeframes or configurations. It also shows the percentage of profits vs losses, and the overall profit/loss for the selected lookback period.

This table serves as a valuable tool for traders to analyze performance and discover optimal settings and timeframes.

The "Smart Money Breakouts" indicator provides traders with a comprehensive solution for breakout trading, combining technical analysis of changes in character and breaks of structure, volume insights, and performance tracking while dynamically adjusting TP and SL levels based on market volatility through the ATR.

This version of the script is a "significant improvement" from Chart Prime's original work in the following ways:

- A selectable range of candles for the profit/loss calculations to look back on.

- An updated table that includes the percentage of wins/losses, and and overall P&L during the selected lookback range.

- The user can now select only Long trades, Short trades, or both.

- The percentage gain/loss is now indicated for every trade on the chart.

- The user can now select a different multiplier for Stop Loss or Take Profit thresholds.

Sector Relative Strength [Afnan]This indicator calculates and displays the relative strength (RS) of multiple sectors against a chosen benchmark. It allows you to quickly compare the performance of various sectors within any global stock market. While the default settings are configured for the Indian stock market , this tool is not limited to it; you can use it for any market by selecting the appropriate benchmark and sector indices.

📊 Key Features ⚙️

Customizable Benchmark: Select any symbol as your benchmark for relative strength calculation. The default benchmark is set to `NSE:CNX100`. This allows for global market analysis by selecting the appropriate benchmark index of any country.

Multiple Sectors: Analyze up to 23 different sector indices. The default settings include major NSE sector indices. This can be customized to any market by using the relevant sector indices of that country.

Individual Sector Control: Toggle the visibility of each sector's RS on the chart.

Color-Coded Plots: Each sector's RS is plotted with a distinct color for easy identification.

Adjustable Lookback Period: Customize the lookback period for RS calculation.

Interactive Table: A sortable table displays the current RS values for all visible sectors, allowing for quick ranking.

Table Customization: Adjust the table's position, text size, and visibility.

Zero Line: A horizontal line at zero provides a reference point for RS values.

🧭 How to Use 🗺️

Add the indicator to your TradingView chart.

Select your desired benchmark symbol. The default is `NSE:CNX100`. For example, use SPY for the US market, or DAX for the German market.

Adjust the lookback period as needed.

Enable/disable the sector indices you want to analyze. The default includes major NSE sector indices like `NSE:CNXIT`, `NSE:CNXAUTO`, etc.

Customize the table's appearance as needed.

Observe the RS plots and the table to identify sectors with relative strength or weakness.

📝 Note 💡

This indicator is designed for sectorial analysis. You can use it with any market by selecting the appropriate benchmark and sector indices.

The default settings are configured for the Indian stock market with `NSE:CNX100` as the benchmark and major NSE sector indices pre-selected.

The relative strength calculation is based on the price change of the sector index compared to the benchmark over the lookback period.

Positive RS values indicate relative outperformance, while negative values indicate relative underperformance.

👨💻 Developer 🛠️

Afnan Tajuddin

Adaptive Linear Regression ChannelOverview

The Adaptive Linear Regression Channel Script is an advanced, multi-functional trading tool crafted to help traders pinpoint market trends, identify potential reversals, assess volatility, and establish dynamic levels for profit-taking and position exits. By incorporating key concepts such as linear regression , standard deviation , and other volatility measures like the ATR , the script offers a comprehensive view of market behavior beyond traditional deviation metrics.

This dynamic model continuously adapts to changing market conditions, adjusting in real-time to provide clear visualizations of trends, channels, and volatility levels. This adaptability makes the script invaluable for both trend-following and counter-trend strategies, giving traders the flexibility to respond effectively to different market environments.

Background

What is Linear Regression?

Definition : Linear regression is a statistical technique used to model the relationship between a dependent variable (target) and one or more independent variables (predictors).

In its simplest form (simple linear regression), the relationship between two variables is represented by a straight line (the regression line).

y = mx + b

where :

- y is the target variable (price)

- m is the slope

- x is the independent variable (time)

- b is the intercept

Slope of the Regression Line

Definition: The slope (m) measures the rate at which the dependent variable (y) changes as the independent variable (x) changes.

Interpretation:

- A positive slope indicates an uptrend.

- A negative slope indicates a downtrend.

Uses in Trading:

- Identifying the strength and direction of market trends.

- Assessing the momentum of price movements.

R-squared (Coefficient of Determination)

Definition: A measure of how well the regression line fits the data, ranging from 0 to 1.

Calculation :

R2 = 1− (SS tot/SS res)

where:

- SSres is the sum of squared residuals.

- SStot is the total sum of squares.

Interpretation:

- Higher R2 indicates a better fit, meaning the model explains a larger proportion of the variance in the data.

Uses in Trading:

- Higher R-squared values give traders confidence in trend-based signals.

- Low R-squared values may suggest that the market is more random or volatile.

Standard Deviation

Definition: Standard Deviation quantifies the dispersion of data points in a dataset relative to the mean. A low standard deviation indicates that data points tend to be close to the mean, while a high standard deviation indicates that the data points are spread out over a larger range of values.

Calculation

σ=√∑(xi−μ)2/N

Where

- σ is the standard deviation.

- ∑ is the summation symbol, indicating that the expression that follows should be summed over all data points.

- xi, this represents the i-th data point in the dataset.

- μ\mu, this represents the mean(average) of all the data points in the dataset.

- (xi−μ)2, this is the squared difference between each data point and the mean.

- N is the total number of data points in the dataset.

- **Interpretation**

- A higher standard deviation indicates greater volatility.

- Useful for identifying overbought/oversold conditions in markets.

Key Features

Dynamic Linear Regression Channels:

The script automatically generates adaptive regression channels that expand or contract based on the current market volatility. This real-time adjustment ensures that traders are always working with the most relevant data, making it easier to spot key support and resistance levels.

The channel width itself serves as an indicator of market volatility, expanding during periods of heightened uncertainty and contracting during more stable phases. Additionally, the channel width is trained on previous channel widths , allowing the script to adapt and provide a more accurate view of volatility trends of the asset. Traders can also customize the script to train on less historical data , enabling a more recent view of volatility , which is particularly useful in fast-moving or changing markets.

Dynamic Profits and Stops:

What is it?

Dynamic profit levels allow traders to adjust take-profit targets based on real-time market conditions. Unlike static levels, which remain fixed regardless of market changes, these adaptive levels leverage past volatility data to create more flexible profit-taking strategies.

How does it work?

The script determines these levels using previously stored deviation values. These deviations are categorized into quantiles (like Q1, Q2, Q3, etc.) to classify current market conditions. As new deviation data is recorded, the profit levels are adjusted dynamically to reflect changes in market volatility. This approach helps to refine profit targets, especially when using regression channels with standard deviation rather than traditional ATR bands.

Why is it valuable?

By utilizing adaptive profit levels, traders can optimize their exits based on the current volatility landscape. For instance, when volatility increases, the dynamic levels expand, allowing trades to capture larger price movements. Conversely, during low volatility, profit targets tighten to lock in gains sooner, reducing exposure to market reversals. This flexibility is especially beneficial when combined with adaptive regression channels that respond to changes in standard deviation.

Slope-Based Trend Analysis:

One of the core elements of this script is the slope of the regression line , which helps define the direction and strength of the trend. Positive slopes indicate bullish momentum, while negative slopes suggest bearish conditions. The slope's steepness gives traders insight into the market's momentum, allowing them to adjust their strategies based on the strength of the trend.

Additionally, the script uses the slope to create a color gradient , which visually represents the intensity of the market's momentum. The gradient peaks at one color to show the maximum bullish momentum experienced in the past, while another color represents the maximum bearish momentum experienced in the past. This color-coded visualization makes it easier for traders to quickly assess the market's strength and direction at a glance.

Volatility Heatmap:

The integrated heatmap provides an intuitive, color-coded visualization of market volatility. The heatmap highlights areas where price action is expanding or contracting, giving traders a clear view of where volatility is rising or falling. By mapping out deviations from the regression line, the heatmap makes it easier to spot periods of high volatility that could lead to major market moves or potential reversals.

Deviation Concepts:

The script tracks price deviations from the regression line when a new range is formed, providing valuable insights when the price significantly deviates from the expected trend. These deviations are key in identifying potential breakout points or trend shifts .

This helps traders understand when the market is overextended or when a pullback may be imminent, allowing them to make more informed trading decisions.

Adaptive Model Properties:

Unlike static indicators, this script adapts over time . As the market changes, it stores historical data related to channel widths , slope dynamics , and volatility levels , adjusting its analysis accordingly to stay relevant to current market conditions.

Traders have the ability to train the model on all available data or specify a set number of bars to focus on more recent market activity. This flexibility allows for more tailored analysis , ensuring that traders can work with data that best fits their trading style and time horizon.

This continuous learning approach ensures that traders always have the most up-to-date insight into the market's structure.

Table

The table displays key metrics in real time to provide deeper insights into market behavior:

1. Deviation & Slope : Shows the current deviation if set to standard deviation or atr if set to atr(values used to calculated the channel widths) and the trend slope, helping to gauge market volatility and trend direction.

2. Rate of Change : For both deviation/atr and slope, the table also calculates the rate of change of their rates—essentially capturing the acceleration or deceleration of trends and volatility. This helps identify shifts in market momentum early.

3. R-squared : Indicates the strength and reliability of the trend fit. A higher value means the regression line better explains the price movements.

4. Quantiles : Uses historical deviation data to categorize current market conditions into quartiles (e.g., Q1, Q2, Q3). This helps classify the market's current volatility level, allowing traders to adjust strategies dynamically.

By combining these metrics, the table offers a comprehensive, real-time snapshot of market conditions, enabling more informed and adaptive trading decisions.

Settings

Here’s a breakdown of the script's settings for easy reference:

Linear Regression Settings

Show Dynamic Levels :Toggle to display dynamic profit levels on the chart.

Deviation Type :Select the method for calculating deviation—options include ATR (Average True Range) or Standard Deviation.

Timeframe :Sets the specific timeframe for the regression analysis (default is the chart’s timeframe).

Period :Defines the number of bars used for calculating the regression line (e.g., 50 bars).

Deviation Multiplier :Multiplier used to adjust the width of the deviation channel around the regression line.

Rate of Change :Sets the period for calculating the rate of change of the slope (used for momentum analysis).

Max Bars Back :Limits the number of historical bars to analyze (0 means all available data).

Slope Lookback :Number of bars used to calculate the slope gradient for trend detection.

Slope Gradient Display :Toggle to enable gradient coloring based on slope direction.

Slope Gradient Colors :Set colors for positive and negative slopes, respectively.

Slope Fill :Adjusts the transparency of the slope gradient fill.

Volatility Gradient Display :Toggle to enable gradient coloring based on volatility levels.

Volatility Gradient Colors :Set colors for low and high volatility, respectively.

Volatility Fill :Adjusts the transparency of the volatility gradient fill.

Table Settings

Show Table :Toggle to display the metrics table on the chart.

Table Position :Choose where to position the table (e.g., top-right, middle-center, etc.).

Font Size :Set the size of the text in the table. Options include Tiny, Small, Normal, Large, and Huge.

AutoCorrelation Test [OmegaTools]Overview

The AutoCorrelation Test indicator is designed to analyze the correlation patterns of a financial asset over a specified period. This tool can help traders identify potential predictive patterns by measuring the relationship between sequential returns, effectively assessing the autocorrelation of price movements.

Autocorrelation analysis is useful in identifying the consistency of directional trends (upward or downward) and potential cyclical behavior. This indicator provides an insight into whether recent price movements are likely to continue in a similar direction (positive correlation) or reverse (negative correlation).

Key Features

Multi-Period Autocorrelation: The indicator calculates autocorrelation across three periods, offering a granular view of price movement consistency over time.

Customizable Length & Sensitivity: Adjustable parameters allow users to tailor the length of analysis and sensitivity for detecting correlation.

Visual Aids: Three separate autocorrelation plots are displayed, along with an average correlation line. Dotted horizontal lines mark the thresholds for positive and negative correlation, helping users quickly assess potential trend continuation or reversal.

Interpretive Table: A table summarizing correlation status for each period helps traders make quick, informed decisions without needing to interpret the plot details directly.

Parameters

Source: Defines the price source (default: close) for calculating autocorrelation.

Length: Sets the analysis period, ranging from 10 to 2000 (default: 200).

Sensitivity: Adjusts the threshold sensitivity for defining correlation as positive or negative (default: 2.5).

Interpretation

Above 50 + Sensitivity: Indicates Positive Correlation. The price movements over the selected period are likely to continue in the same direction, potentially signaling a trend continuation.

Below 50 - Sensitivity: Indicates Negative Correlation. The price movements show a likelihood of reversing, which could signal an upcoming trend reversal.

Between 50 ± Sensitivity: Indicates No Correlation. Price movements are less predictable in direction, with no clear trend continuation or reversal tendency.

How It Works

The indicator calculates the logarithmic returns of the selected source price over each length period.

It then compares returns over consecutive periods, categorizing them as either "winning" (consistent direction) or "losing" (inconsistent direction) movements.

The result for each period is displayed as a percentage, with values above 50% indicating a higher degree of directional consistency (positive or negative).

A table updates with descriptive labels (Positive Correlation, Negative Correlation, No Correlation) for each tested period, providing a quick overview.

Visual Elements

Plots:

AutoCorrelation Test : Displays autocorrelation for the closest period (lag 1).

AutoCorrelation Test : Displays autocorrelation for the second period (lag 2).

AutoCorrelation Test : Displays autocorrelation for the third period (lag 3).

Average: Displays the simple moving average of the three test periods for a smoothed view of overall correlation trends.

Horizontal Lines:

No Correlation (50%): A baseline indicating neutral correlation.

Positive/Negative Correlation Thresholds: Dotted lines set at 50 ± Sensitivity, marking the thresholds for significant correlation.

Usage Guide

Adjust Parameters:

Select the Source to define which price metric (e.g., close, open) will be analyzed.

Set the Length based on your preferred analysis window (e.g., shorter for intraday trends, longer for swing trading).

Modify Sensitivity to fine-tune the thresholds based on market volatility and personal trading preference.

Interpret Table and Plots:

Use the table to quickly check the correlation status of each lag period.

Analyze the plots for changes in correlation. If multiple lags show positive correlation above the sensitivity threshold, a trend continuation may be expected. Conversely, negative values suggest a potential reversal.

Integrate with Other Indicators:

For enhanced insights, consider using the AutoCorrelation Test indicator in conjunction with other trend or momentum indicators.

This indicator offers a powerful method to assess market conditions, identify potential trend continuations or reversals, and better inform trading decisions. Its customization options provide flexibility for various trading styles and timeframes.

Weekly High/Low Day BreakdownThe "Weekly High/Low Day Breakdown" is a tool designed to help identify patterns in market behaviour by analysing the days of the week when weekly highs and lows occur. This indicator calculates the frequency and percentage of weekly highs and lows for each day from Monday to Sunday within the visible range of your chart.

Features:

Weekly Analysis: Calculates weekly highs and lows based on daily open high and low prices from Monday to Sunday.

Day-Specific Breakdown: Tracks which day of the week each weekly high and low occurred.

Visible Range Focus: Only considers data within the current visible range of your chart for precise analysis.

Interactive Table Display: Presents the results in an easy-to-read table directly on your chart.

How It Works:

Data Collection: Fetches daily high, low, day of the week, and time data regardless of your chart's timeframe. Uses these daily figures to determine the weekly high and low for each week.

Weekly Tracking: Monitors the day of the week when the weekly high and low prices occur. Resets tracking at the end of each week (Sunday).

Visible Range Analysis: Only includes weeks that fall entirely within the visible time range of your chart. Ensures that the analysis is relevant to the period you are focusing on.

Percentage Calculation: Counts the occurrences of weekly highs and lows for each day. Calculates the percentage based on the total number of weeks in the visible range.

Result Display: Generates a table with days of the week as columns and "Weekly High" and "Weekly Low" as rows. Displays the percentage values, indicating how often highs and lows occur on each day.

How to Use:

Add the Indicator: Apply the "Weekly High/Low Day Breakdown" indicator to your TradingView chart.

Adjust Visible Range: Zoom in or out to set the desired visible time range for your analysis.

Interpret the Table:

Columns: Represent days from Monday to Sunday.

"Weekly High" Row: Shows the percentage of times the weekly high occurred on each day. "Weekly Low" Row: Shows the percentage of times the weekly low occurred on each day.

Colors: Blue text indicates high percentages, red text indicates low percentages.

Example Interpretation:

If the table shows a 30% value under "Tuesday" for "Weekly High," it means that in 30% of the weeks within the visible range, the highest price of the week occurred on a Tuesday.

Similarly, a 40% value under "Friday" for "Weekly Low" indicates that 40% of the weekly lows happened on a Friday.

RV- Dynamic Trend AnalyzerRV Dynamic Trend Analyzer

The RV Dynamic Trend Analyzer is a powerful TradingView indicator designed to help traders identify and capitalize on trends across multiple time frames—daily, weekly, and monthly. With dynamic adjustments to key technical indicators like EMA and MACD, the tool adapts to different chart periods, ensuring more accurate signals. Whether you are swing trading or holding longer-term positions, this indicator provides reliable buy/sell signals, breakout opportunities, and customizable visual elements to enhance decision-making. Its intelligent use of EMAs and MACD values ensures high potential returns, making it suitable for traders seeking strong, data-driven strategies. Below are its core features and their respective benefits.

Supertrend Indicator:

Importance: The Supertrend is a trend-following tool that helps traders identify the market’s direction by offering clear buy and sell signals based on price movement relative to the Supertrend line.

Benefits:

Helps filter out market noise and enables traders to stay in trends longer.

The pullback detection feature enhances trade timing by identifying potential entry points during retracements.

ATH/ATL & 52-Week High/Low with Candle Coloring:

Importance: Tracking all-time highs (ATH), all-time lows (ATL), and 52-week high/low levels helps traders identify key support and resistance levels.

Benefits:

Offers insights into the strength of price movements and potential reversal zones.

Candle coloring improves visual analysis, allowing quick identification of bullish or bearish conditions at critical levels.

Multi-Time Frame Analysis

Importance: The ability to view indicators like RSI and MACD across multiple time frames provides a more in-depth and comprehensive view of market behavior, allowing traders to make informed decisions that align with both short-term and long-term trends.

Benefits:

Align Strategies Across Time frames: By using multiple time frames, traders can align their strategies with larger trends (such as weekly or daily) while executing trades on lower time frames (like 1-minute or 5-minute charts). This improves the accuracy of trade entries and exits.

Reduce False Signals: Viewing key technical indicators like RSI and MACD across different time frames reduces the likelihood of false signals by offering a broader market context, filtering out noise from smaller time frames.

Customization of Table Display: Traders can customize the position and size of a table that displays RSI and MACD values for selected time frames. This flexibility enhances visibility and ease of analysis.

Time frame-Specific Data: The code allows for displaying RSI and MACD data for up to seven different time frames, making it highly customizable for traders depending on their preferred analysis period.

Visual Clarity: The table displays key values such as RSI and MACD histogram readings in a visually clear format, with color coding to quickly indicate overbought/oversold levels or MACD crossovers.

Pivot Points:

Importance: Pivot points serve as key support and resistance levels that help predict potential price movements.

Benefits:

Assists in identifying potential reversal zones and breakout points, aiding in trade planning.

Displaying pivot points across multiple time frames enhances market insight and improves strategic planning.

Quarterly Earnings Table:

Importance: Understanding a company’s quarterly earnings releases is crucial, as these events often lead to significant price volatility. Traders can leverage this information to adjust their strategies around earnings reports and prevent unexpected losses.

Benefits:

Helps traders anticipate potential price movements due to earnings reports.

Allows traders to avoid sudden losses by being aware of important earnings announcements and adjusting positions accordingly.

Customizable Visuals for Traders:

Dark Mode: Toggle between dark and light themes based on your chart's color scheme.

Mini Mode: A condensed version that visually simplifies the data, making it quicker to interpret through color-coded traffic lights (green for positive, red for negative).

Table Size & Position: Customize the size and position of the table for better visibility on your charts.

Data Period (FQ vs FY): Easily switch between displaying quarterly or yearly data based on the selected period.

Top-Left Cell Display: Option to display Free Float or Market Cap in the top-left cell for quick reference.

Exponential Moving Averages (EMAs) with Adjustable Lengths:

Importance: EMAs are essential for identifying trends and generating reliable buy/sell signals. The indicator plots four EMAs that dynamically adjust based on the selected time frame.

Benefits:

Dynamic Time frame Logic: EMA lengths and sources automatically adapt based on whether the user selects daily, weekly, or monthly time frames. This ensures the EMAs are relevant for the chosen strategy.

Multiple EMAs: By incorporating four different EMAs, users can observe both short-term and long-term trends simultaneously, improving their ability to identify key trend shifts.

Breakout Arrow Functionality:

Importance: This feature visually signals potential buy/sell opportunities based on the interaction between EMAs and MACD crossovers.

Benefits:

Crossover Signals: Arrows are plotted when EMAs and MACD cross, indicating breakout opportunities and aiding in quick trade decisions.

RSI Filter Option: Users can apply an optional RSI filter to refine buy/sell signals, reducing false signals and improving overall accuracy.

Disclaimer:

Before engaging in actual trading, we strongly recommend back testing the this indicator to ensure it fits your trading style and risk tolerance. Be sure to adjust your risk-reward ratio and set appropriate stop-loss levels to safeguard your investments. Proper risk management is key to successful trading.

Memecoin TrackerMemecoin Z-Score Tracker with Buy/Sell Table - Technical Explanation

How it Works:

This indicator calculates the Z-scores of various memecoins based on their price movements, using historical funding rates across multiple exchanges. A Z-score measures the deviation of the current price from its moving average, expressed in standard deviations. This provides insight into whether a coin is overbought (positive Z-score) or oversold (negative Z-score) relative to its recent history.

Key Components:

- Z-Score Calculation

- The lookback period is dynamically adjusted based on the chart’s timeframe to ensure consistency across different time intervals:

- For lower timeframes (e.g., minutes), the base lookback period is scaled to match approximately 240 minutes.

- For daily and higher timeframes, the base lookback period is fixed (e.g., 14 bars).

Memecoin Selection:

The indicator tracks several popular memecoins, including DOGE, SHIB, PEPE, FLOKI, and others.

Funding rates are fetched from exchanges like Binance, Bybit, and MEXC using the request.security() function, ensuring accurate real-time price data.

Thresholds for Buy/Sell Signals:

Users can set custom Z-score thresholds for buy (oversold) and sell (overbought) signals:

Default upper threshold: 2.5 (indicates overbought condition).

Default lower threshold: -2.5 (indicates oversold condition).

When a memecoin’s Z-score crosses above or below these thresholds, it signals potential buy or sell conditions.

Buy/Sell Table:

A table with two columns (BUY and SELL) is dynamically populated with memecoins that are currently oversold (buy signal) or overbought (sell signal).

Each column can hold up to 20 entries, providing a clear overview of current market opportunities.

Visual Feedback:

The Z-scores of each memecoin are plotted as a line on the chart, with color-coded feedback:

Red for overbought (Z-score > upper threshold),

Green for oversold (Z-score < lower threshold),

Other colors indicate neutral conditions.